Family Limited Partnerships & Limited Liability Companies:

Powerful Advanced Estate Planning Tools

Most estate plans focus on transferring assets after death. Advanced estate planning, however, seeks to accomplish much more—it helps preserve family wealth, minimize taxes, protect assets, and facilitate the orderly transfer of wealth from one generation to the next.

For families with substantial assets, closely held businesses, investment real estate, or valuable investment portfolios, a Family Limited Partnership (FLP) or Family Limited Liability Company (Family LLC) may be an effective planning strategy.

Although these entities are not appropriate for every family, they can provide significant estate planning, asset protection, and business succession benefits when properly designed and maintained.

What Is a Family Limited Partnership?

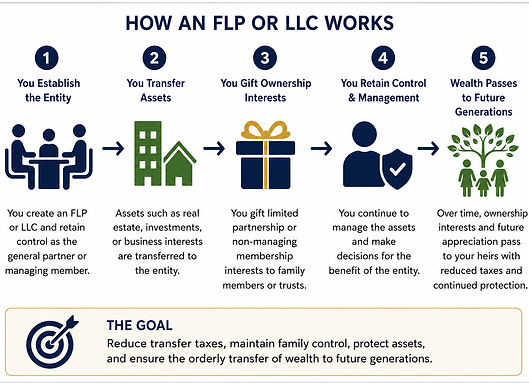

A Family Limited Partnership (FLP) is a legal entity that allows family members to own interests in assets through a partnership structure.

Typically, the parents serve as the General Partners, retaining management and control over the partnership's assets.

Children or other family members often receive Limited Partnership Interests, allowing them to share in the economic benefits of the partnership without participating in day-to-day management.

This structure enables parents to gradually transfer wealth while maintaining control over the family's investments and business affairs.

What Is a Family LLC?

A Family Limited Liability Company (Family LLC) accomplishes many of the same objectives but uses the more familiar LLC structure.

Parents often serve as the Managing Members, while children receive non-managing membership interests.

Like an FLP, a Family LLC allows senior family members to retain control over investment decisions while transferring ownership interests to younger generations over time.

Many families prefer the LLC structure because it is more flexible and familiar to business owners.

How Do FLPs and Family LLCs Work?

Instead of transferring individual assets directly to children or other beneficiaries, parents transfer assets into the FLP or Family LLC.

These assets may include:

-

investment real estate;

-

rental properties;

-

marketable securities;

-

closely held business interests;

-

farms and ranches;

-

family vacation properties; and

-

other investment assets.

Parents then begin gifting minority ownership interests to children or trusts for their benefit while continuing to manage the assets themselves.

This allows wealth to be transferred gradually without relinquishing control.

Estate Tax Benefits

One of the primary advantages of FLPs and Family LLCs is the ability to transfer ownership interests rather than individual assets.

Because minority ownership interests generally lack control over the entity and cannot easily be sold on the open market, qualified appraisers may determine that these interests are worth less than a proportional share of the underlying assets. These valuation discounts may reduce the taxable value of gifts and estates for federal transfer tax purposes.

These strategies are highly technical and must be supported by appropriate appraisals and careful planning.

Asset Protection Benefits

When properly established and operated, FLPs and Family LLCs may also provide a measure of asset protection.

Although no planning strategy can eliminate every risk, these entities may make it more difficult for certain creditors to reach family assets while promoting centralized management and long-term preservation of wealth.

Asset protection planning should always be implemented before creditor issues arise and should never be used to hinder, delay, or defraud creditors.

Business Succession Planning

Family businesses often fail because there is no succession plan.

An FLP or Family LLC can create a clear ownership structure that allows younger family members to gradually become involved in the business while senior family members continue making management decisions.

Over time, ownership interests may be transferred to the next generation without disrupting daily operations.

Advantages of Family Limited Partnerships and Family LLCs

A properly structured FLP or Family LLC may:

-

facilitate the transfer of wealth to future generations;

-

allow parents to retain management control;

-

provide opportunities for valuation discounts for federal transfer tax purposes;

-

centralize management of family assets;

-

simplify business succession planning;

-

encourage long-term family ownership of investment assets;

-

provide certain asset protection benefits; and

-

help reduce family disputes through clearly defined ownership and management provisions.

Important Considerations

These planning strategies are not "do-it-yourself" projects.

To achieve the intended tax and legal benefits, an FLP or Family LLC must be operated as a legitimate business entity.

That generally includes:

-

maintaining separate bank accounts;

-

keeping accurate books and records;

-

documenting meetings and significant decisions when appropriate;

-

respecting entity formalities;

-

obtaining qualified appraisals when valuation discounts are claimed; and

-

avoiding the use of the entity solely as a tax avoidance device.

Failure to properly operate the entity can significantly reduce—or even eliminate—the intended benefits.

Is an FLP or Family LLC Right for You?

Family Limited Partnerships and Family LLCs are sophisticated estate planning tools designed for families with significant assets or closely held businesses.

For many families, a Revocable Living Trust and other traditional estate planning documents provide all the planning they need.

However, if you own substantial investment assets, a family business, commercial real estate, or other appreciating property, an FLP or Family LLC may provide valuable tax planning, asset protection, and succession planning opportunities.

Choosing the right strategy requires careful coordination with your estate plan, tax advisor, and overall financial goals. An experienced Florida estate planning attorney can help determine whether an FLP or Family LLC is appropriate for your family's unique circumstances.